Financial Statement II (With Adjustments)

- Needs for Adjustments in Preparing the Final Accounts

The purpose of making various adjustments is to ensure that the final accounts must reveal the true profit or loss and true financial position of the business.

- It helps us to record those adjustment which were left or committed and were not recorded in the accounts.

- A proper recording of adjusting entries assists us to separate all the financial transactions into a year-wise category.

- Recording of adjusting entries provides us the room for making various provisions which are made at the end of year, after assessing the entire year’s performance.

The Item which Usually Need Adjustments

- Closing stock

Accounting Treatment

| Adjusting Entry | Trading Account | Balance Sheet |

| Closing Stock A/c Dr

To Trading A/c (Being the closing stock recorded in the books) |

Shown on the credit side. | Shown on the assets side under current assets. |

- Outstanding Expenses

Accounting Treatment

| Adjusting Entry | Trading Account | Profit and Loss Account | Balance Sheet |

| Concerned Expenses A/c Dr

To Outstanding Expenses A/c (Being the unpaid expenses provided) |

(If it is a direct expenses, e.g. wages)

Added to the concerned expenses on the debit side. |

(If it is an indirect expenses, e.g. salaries)

Added to the concerned expenses on the debit side. |

Shown on the liabilities side as a current liability. |

- Prepaid/Unexpired Expenses

Accounting Treatment

| Adjusting Entry | Trading Account | Profit and Loss Account | Balance Sheet |

| Prepaid

Expenses A/c Dr To Concerned Expenses A/c (Being concerned expenses paid in advance) |

(If it is a direct expenses, e.g. wages)

Deducted from the concerned expenses on the debit side. |

(If it is an indirect expenses, e.g. insurance premium)

Deducted from the concerned expenses on the debit side. |

Shown on the assets side as a current assets. |

Accrued Income

Accounting Treatment

| Adjusting Entry | Profit and Loss Account | Balance Sheet |

| Accrued Income A/c Dr

To Concerned Income A/c (Being concerned income receivable) |

Added to the respective income on the credit side. | Shown on the assets side as a current asset. |

- Income received in Advance

Accounting Treatment

| Adjusting Entry | Profit and Loss Account | Balance Sheet |

| Concerned Income A/c Dr

To Income Received in Advance A/c (Being adjustment for unearned income) |

Deducted from the concerned income on the credit side. | Shown on the liabilities side. |

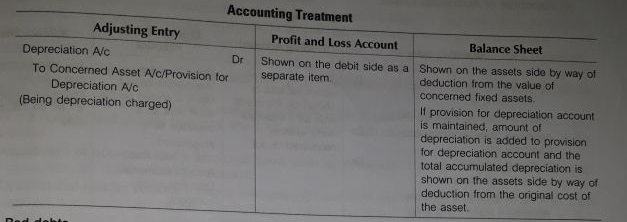

- Depreciation

Accounting Treatment

- Bad debts

Accounting Treatment

- Provision for doubtful debts

Accounting Treatment

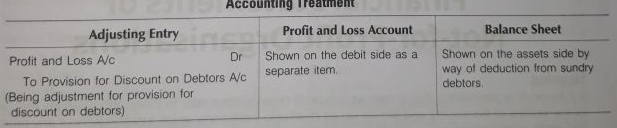

- Provision for discount on debtors

Accounting Treatment

- Manager’s Commission

Accounting Treatment

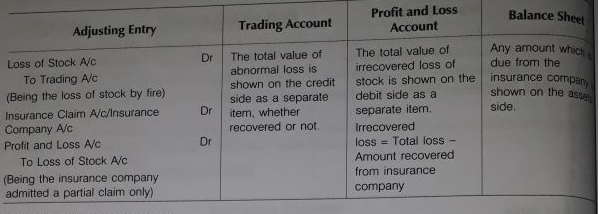

- Abnormal or Accidental Losses

Accounting Treatment

- Goods taken for personal use

Accounting Treatment

- Goods distributed as free samples

Accounting Treatment

Thank u so much for giving me this notes .They are very helpful.